Solar Panel Leasing Pros and Cons: A Clear Side-by-Side Guide

An objective, data-driven analysis of solar panel leasing pros and cons, comparing lease vs purchase to help homeowners decide on the most cost-effective solar financing.

Leasing solar panels can reduce upfront costs and simplify maintenance, but it often yields lower long-term savings and transfers production incentives to the lessor. The right choice depends on your long-term plans, credit situation, and ability to take advantage of incentives or utility programs. Below, we compare leased vs purchased systems to help you decide.

Why solar panel leasing pros and cons matter for homeowners

According to Solar Panel FAQ, understanding the decision to lease solar panels is essential for homeowners who want to go solar without large upfront costs. The phrase solar panel leasing pros and cons captures the core trade-offs between renting access to solar generation and owning the system outright. In practice, leasing reduces your initial investment and shifts maintenance and performance risk to the lease provider, which can simplify budgeting and remove maintenance headaches. However, it can limit your ability to claim tax incentives, claim production credits, or upgrade the system to newer technology. Solar Panel FAQ analysis shows that many households face a trade-off between predictable monthly payments and the potential for greater lifetime savings with ownership. The decision hinges on how long you expect to remain in the home, your energy usage patterns, your credit quality, and the specifics of local incentives, which vary by utility territory and state policy. As a result, a side-by-side comparison is essential before committing to a contract.

How solar panel leasing works

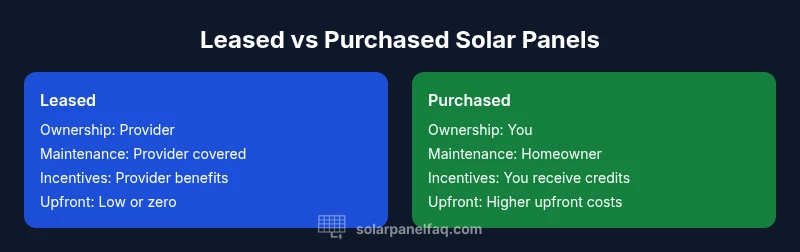

Solar panel leasing is a financing arrangement where a solar company owns the photovoltaic system installed on your home. You pay a fixed monthly lease payment and benefit from reduced electric bills based on the system’s output. The lease may include an annual escalator, which increases your payment over time, and a guaranteed level of performance. At the end of the term, you typically have options such as purchasing the system, renewing the lease, or having the panels removed. Because the lessor owns the hardware, maintenance and repairs are often covered under the lease agreement, reducing your ongoing responsibility. However, the provider generally claims any remaining incentives and tax credits, which can affect the total value you realize.

Key financial considerations when choosing leasing over buying

From a financial standpoint, the core question is whether the sum of fixed lease payments plus any residual costs is lower than the long-term savings from owning a system. Leasing usually has no or low upfront costs, offering predictable monthly expenses. However, the total lifetime cost can be higher than buying when incentives, depreciation, and potential energy savings are considered. It’s important to review the annual escalator (if any), the buyout option at term end, and how the lease affects your utility rate reductions. When comparing offers, compute two scenarios: (1) leasing with fixed payments and potential end-of-lease buyout, and (2) purchasing with a loan and the option to keep or sell the system later. The goal is to estimate break-even timelines and determine which path delivers the best financial return given your time horizon and electricity usage.

Maintenance, warranties, and service expectations

A key practical difference between leasing and ownership is who handles maintenance and repairs. In most leases, the provider takes responsibility for system performance, cleaning, and component replacements under warranty terms, reducing homeowners’ hands-on duties. This can be appealing for homeowners who want a hands-off solar experience. Warranties typically cover the panels and inverters, but the terms vary by provider. When evaluating offers, confirm exactly which components are covered, for how long, and what counts as a failure. Also verify response times for service calls and whether there are any out-of-pocket costs for non-warranty issues. Clear, written service level agreements protect against surprise charges and ensure you receive consistent, reliable performance.

Incentives, tax credits, and policy considerations

In a lease, incentives and tax credits typically flow to the lessor rather than the lessee. This can reduce the perceived value of the investment for you, the homeowner, since the lease price reflects these incentives indirectly. It is essential to understand how local incentives, performance-based incentives, and state policies interact with your lease. Some programs allow the lessee to take advantage of net metering credits or time-of-use rates, but this varies widely by jurisdiction. When comparing offers, request a side-by-side breakdown of which incentives the provider claims and how those savings are reflected in your monthly payments or buyout price. You may also encounter program changes during the lease term that could impact overall economics.

Risk and performance considerations

Performance risk is another critical factor. If solar production underperforms due to shading, soiling, or aging components, a lease may limit your ability to capture the full value of the installed system. In contrast, a purchased system usually aligns incentives with the homeowner’s outcomes, since they own the asset and benefit directly from any performance gains or lower utility costs. Carefully review the projected output guarantees, the certification of equipment, and what happens if the system underperforms. Also consider the risk of early termination or relocation: some leases allow for transfer to a new owner, while others impose penalties. Understanding these conditions can prevent costly surprises.

Leasing vs buying: Long-term economics and payback

The long-term economics of leasing versus buying hinge on how long you stay in the home, your electricity usage trajectory, and the local price of solar energy. Leases offer predictable, lower upfront costs and simplified budgeting, but ownership generally yields higher lifetime savings and eligibility for tax incentives. Use a calculator or an advisor to model cash flows over the lease term and compare them with a purchasing scenario that includes loan payments, depreciation, and potential resale value of the system. If you anticipate moving within the lease term or expect significant advances in solar technology, leasing can be attractive. Otherwise, purchase may provide greater total value over the system’s lifetime.

Best scenarios: When leasing makes sense

Leasing can be a strong choice for homeowners who: (a) want to minimize upfront costs; (b) plan to move within the lease term; (c) prefer a turnkey, maintenance-included solution; or (d) have credit constraints that make loan-based financing less attractive. Leasing is less favorable for homeowners who expect to stay long-term in the property, expect to take full advantage of tax credits and depreciation, or want maximum control over system upgrades and performance improvements. In markets with strong incentives and dynamic electricity pricing, purchasing can outperform leasing in the long run. Always compare the full lifecycle costs and consider potential changes in energy usage and policy.

How to evaluate a solar leasing proposal: a practical checklist

When reviewing offers, use a structured checklist: (1) confirm ownership and end-of-term options; (2) compare monthly payments, escalators, and total payout; (3) verify maintenance commitments and response times; (4) identify who claims incentives and how they affect your net savings; (5) assess end-of-term buyout options and potential removal costs; (6) request a production forecast with a confidence interval; (7) read the contract for early termination terms; (8) confirm compatibility with future system upgrades and backup storage, if desired. A careful review reduces surprises and helps align the deal with your long-term goals.

End-of-term decisions and options

As leases mature, you’ll often face a decision: exercise an upfront buyout to own the panels, renew the lease, or have the system removed. Each option has financial and practical implications, including asset ownership, potential resale value, and future energy costs. If you expect electricity prices to rise, owning the system can lock in long-term energy savings even if the initial payments are higher. If you plan to move soon, leasing may offer an easier transition, but ensure the contract allows a smooth transfer of obligations to a new homeowner. A well-structured lease also leaves open the possibility of upgrading to newer solar technology in the future.

Final thoughts

Choosing between leasing and buying solar panels requires weighing upfront costs, long-term savings, incentives, and your plans for the home. A disciplined, apples-to-apples comparison helps you avoid biased assessments driven by marketing language. The goal is to maximize value for your household over the time you expect to remain in the property while maintaining flexibility as energy markets evolve.

Comparison

| Feature | Leased solar panels | Purchased solar panels |

|---|---|---|

| Ownership at end of term | Lessee does not own the hardware; ownership remains with the lessor | Homeowner owns the system outright (or via loan) if purchased |

| Maintenance responsibility | Lessor typically handles maintenance and repairs under lease terms | Owner responsible for maintenance and repairs after purchase |

| Incentives and tax credits | Incentives and tax credits usually go to the lessor | Homeowner receives incentives and depreciation benefits |

| Monthly cost structure | Fixed monthly lease payments (plus potential escalator) | Loan payment (if financed) plus ongoing energy costs; potential savings from ownership |

| Performance risk | Performance risk largely borne by the provider; guaranteed output is typical | Owner bears performance risk, but gains direct savings from reduced bills |

| End-of-term options | Purchase option or lease renewal; removal costs may apply | Option to buy, keep generating, or upgrade; removal costs depend on sale terms |

| Long-term economics | Typically lower upfront cost; total lifetime value may be lower | Higher upfront or financed cost; higher total lifetime value with incentives |

Strengths

- Lower upfront costs and easier approval for homeowners with limited cash

- Predictable monthly payments that simplify budgeting

- Maintenance and repairs are often covered by the provider

- No immediate large capital expenditure or ownership hassles

Drawbacks

- Lower total lifetime savings compared with ownership

- Incentives and tax credits go to the lessor, not the homeowner

- End-of-term costs or renewals may increase long-term expenses

- Less control over system upgrades and customization

Buying is generally more cost-effective in the long run for homeowners who plan to stay long-term and want maximum incentives; leasing shines for short tenures or those seeking minimal upfront costs.

Lease offers budget-friendly entry into solar with maintenance included, but ownership yields greater lifetime savings and policy benefits. If you expect to stay long enough for payback and want full incentives, buying is usually preferable; otherwise, leasing can be a sensible bridge to solar.

Frequently Asked Questions

What is solar panel leasing, and how does it differ from buying?

Solar panel leasing is an arrangement where a provider owns and maintains the solar system, and you pay a fixed monthly lease. Buying means you own the system either with cash or a loan. Leasing typically offers lower upfront costs, while buying can yield greater long-term savings and tax incentives.

Solar leasing means you lease the panels from a provider who maintains them; buying means you own the system. Leasing lowers upfront costs, but buying usually saves more in the long run and lets you claim incentives.

Do I still qualify for tax credits if I lease solar panels?

In most leases, the tax credits and incentives go to the lessor rather than you. This doesn’t mean you can’t benefit from solar energy; you’ll still see reduced electricity bills, but the financial upside comes through lower lease payments rather than credits.

Usually, tax credits go to the lease provider. You still save on bills, but incentives are not directly yours.

What happens at the end of a solar lease?

At the end of a lease term, you typically have options such as buying the system, renewing the lease, or having the panels removed. The availability and cost of a buyout or upgrade depend on your contract terms.

End of term options usually include buyout, renewal, or removal; terms vary by contract.

Is leasing always the cheaper option in the long term?

Not always. Leasing can reduce upfront costs, but total lifetime costs may be higher than buying when incentives and depreciation are considered. A careful cash-flow analysis helps determine which path saves money over the system’s life.

Leasing isn’t always cheaper long-term; compare total costs over the system’s life.

How do I evaluate a solar leasing proposal?

Use a structured checklist: ownership terms, monthly payment, escalators, maintenance coverage, incentives allocation, end-of-term options, and performance guarantees. Request independent third-party projections and compare against a purchase scenario.

Review ownership, payments, incentives, and end-of-term options; compare with buying.

Top Takeaways

- Evaluate long-term stay plans before choosing leasing

- Consider who benefits from incentives in each option

- Account for maintenance, buyout options, and end-of-term costs

- Run side-by-side cash flow analyses for apples-to-apples comparison

- Ask for transparent, written guarantees on production and service