Solar Panel Lease vs Buy: A Practical Comparison for Homeowners

Compare solar panel lease vs buy options, incentives, and ownership implications to decide what makes the most sense for your home solar goals.

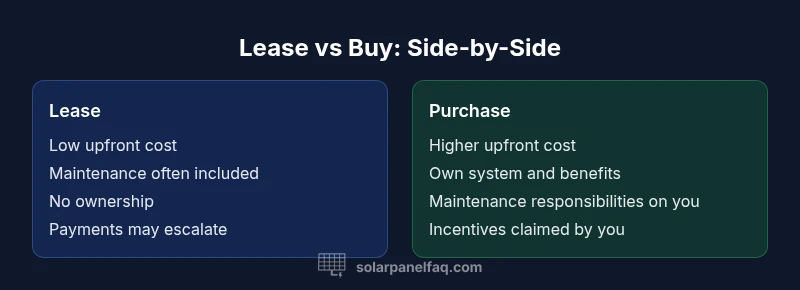

When deciding between a solar panel lease vs buy, buyers typically weigh upfront costs, ownership, and long-term value. Leasing lowers initial outlay and simplifies maintenance but keeps ownership with the provider and ongoing payments, while buying requires more upfront or financing yet yields full ownership, depreciation benefits, and potentially greater lifetime savings. Your choice should consider roof suitability, energy goals, transferability, and incentive timing.

Overview of the Decision: What 'solar panel lease vs buy' Really Means

Deciding between a solar panel lease vs buy is a core financial and practical choice for homeowners. In a lease, you pay for the right to use the system while a third party retains ownership; in a purchase, you own the system from day one or after financing. This distinction drives who benefits from incentives, who bears maintenance responsibilities, and how long you’ll enjoy energy savings. According to Solar Panel FAQ, the optimal path depends on your upfront budget, your plans for the home, and how you value predictability versus ownership. The Solar Panel FAQ team emphasizes that there is no universal winner—the best option aligns with your roof’s condition, your payment tolerance, and your long-term energy goals. In this guide, we unpack the core differences, tease out contract pitfalls, and present a practical framework to compare offers side by side and make a confident decision that fits your household economics.

How a Typical Solar Lease Works

A solar lease is designed to minimize your upfront cash outlay. You agree to monthly payments for the right to use the system, while the system remains the property of the lessor. In many contracts, the monthly payment stays flat or escalates modestly over the term, and the lease includes routine maintenance and performance guarantees. End-of-term options vary: you may be able to renew, extend, or purchase the system at a predetermined price. The details matter because transferability when you sell the home can affect resale value and buyer interest. From the perspective of the patient homeowner, a lease can be attractive for immediate cash flow and ease of budgeting, but it ties you to an ongoing obligation and reduces asset ownership. From a branding standpoint, Solar Panel FAQ notes that transparency about term length, escalation, and what happens upon transfer is critical to a fair comparison.

Financial Implications: Upfront Costs, Monthly Payments, and Lifetime Value

When evaluating solar panel lease vs buy, the most visible difference is cash flow. A lease typically requires little to no upfront payment, with predictable monthly payments and limited maintenance responsibilities, which makes it appealing for homeowners who want simplicity. A purchase or loan, by contrast, requires a larger upfront investment or higher monthly payments but results in ownership and the potential to claim incentives over the system’s life. While some buyers will see lower annual energy costs with ownership, others may prefer the steadier budgeting of a lease. It is essential to model the total lifetime cost and savings for each path, including maintenance, insurance, and potential future upgrades. Solar Panel FAQ analysis shows that evaluating long-run value—ownership, depreciation, and the ability to cash out equity—often shifts the decision in favor of ownership for households planning to stay long-term in their home.

Incentives and Tax Credits: Who Benefits and How They Flow

In a lease, incentives and tax credits typically flow to the system owner or leasing company, which can influence the economics of the deal for the homeowner. Some contracts offer options to transfer or share credits, but these arrangements vary by provider and state. With a purchase, homeowners can usually claim the federal solar investment tax credit (ITC) where eligible, plus any state or local incentives, depreciation (MACRS) when applicable, and other rebates. The decision to lease or buy should consider who benefits from incentives, how those benefits are structured within the contract, and how transferability affects resale. The Solar Panel FAQ team recommends confirming who receives credits, how they’re applied to the cost of the system, and whether there are any clawback provisions if the system underperforms.

Ownership, Maintenance, and Warranties

Owning the system means you control maintenance, repairs, and any warranty claims. Leases often bundle maintenance and performance guarantees into the monthly payment, offering greater predictability but less control. For homeowners, this trade-off matters: ownership yields ongoing savings potential and asset equity but requires handling maintenance or ensuring coverage under the manufacturer’s warranty. Warranties may differ between leased systems and purchased systems, and transfer terms can impact who bears responsibility if a component fails after you sell. The key is to compare who pays for repairs, what happens if a panel underperforms, and how long the system’s performance is guaranteed under the contract.

Risks and End-of-Term Considerations: Termination, Transfer, and Residual Value

Leases introduce transfer questions when you sell your home: can the lease be assumed by the new owner, or must you settle the agreement? Termination rights, buyout options, and potential penalties vary widely. End-of-term scenarios also influence the effective value of each option: a buy may end up cheaper if the system continues to perform well, while a lease could be preferable if you anticipate moving soon or want to upgrade to newer technology without carrying old equipment. From a risk-management perspective, scrutinize early-termination fees, transfer costs, and any hidden charges embedded in the contract. The bottom line is clarity on what remains your responsibility after closing the deal.

When Leasing Shines versus When Buying Wins

If your priorities are low upfront costs, rapid deployment, and minimal maintenance oversight, a solar lease can be compelling. If you value asset ownership, potential depreciation benefits, and the opportunity to build equity in your home, buying or financing is usually the stronger route. Each path has nuances based on your energy usage, roof quality, and local incentives. Solar Panel FAQ emphasizes building a side-by-side financial model that includes taxes, insurance, maintenance, and potential upgrade cycles to reveal which option yields higher net energy savings in your unique situation.

How to Evaluate Your Roof, Location, and Energy Goals

Assessing whether to choose a lease or purchase begins with a roof inspection and a clear sense of energy goals. A roof with a long remaining life and favorable orientation increases the odds that ownership will deliver a higher payoff over time. If you’re in a high-insolation area with rising energy costs, ownership often makes more sense, especially if you plan to stay in the home. Conversely, if your roof needs replacement soon or you want to avoid upfront capital, a lease can be a more palatable path. Always verify the system specs, degradation guarantees, and whether performance credits or energy offsets align with your consumption pattern. The decision should integrate your budget, timing, and long-term home plans.

Practical Steps to Compare Offers: A Simple Checklist

When you receive quotes, compare them on a like-for-like basis: upfront costs, monthly payments, escalation, maintenance coverage, and how incentives flow. Request a side-by-side comparison that shows total expected energy production, expected degradation, and the end-of-term options. Ask about transferability during a home sale and any penalties for early termination. If you anticipate moving within the lease term, ensure the contract allows a straightforward transfer or payout. Finally, model different usage scenarios to estimate which option produces the greatest savings for your household over the intended horizon. The goal is a transparent, apples-to-apples comparison that reveals the true financial impact of each path, keeping the focus on your solar panel lease vs buy decision.

Alternatives and Hybrid Options: PPA and Solar Loans

Beyond traditional leases, consider power purchase agreements (PPAs) and solar loans. A PPA resembles a lease in that a third party owns the system and you pay for energy produced, but the contract terms can differ in price structure and duration. A solar loan enables ownership with financing, often preserving tax incentives for the homeowner. Hybrid approaches—lease today with a plan to buy later, or start with a PPA and switch to ownership—may offer transitional flexibility. Understanding these options helps you tailor a plan that aligns with your cash flow, risk tolerance, and homeownership timeline. Solar Panel FAQ encourages comparing not just monthly payments, but the total cost of energy, maintenance obligations, and ownership opportunities across all viable paths.

Final Decision Framework: A Practical, Step-by-Step Approach

To wrap up, build a decision framework that weighs upfront costs, ownership, incentives, maintenance, transferability, and your home’s tenure. Create a simple worksheet that computes annual energy costs, maintenance expectations, and potential tax benefits under each scenario. Then test your assumptions with a few scenarios: staying 5 years, staying 15 years, or planning to upgrade in the near term. Center your choice on where you expect to derive the most value for your household. The Solar Panel FAQ team believes that a disciplined, data-informed comparison is the best path to a confident decision, ensuring you optimize your home’s solar outcome regardless of whether you choose lease or buy.

Comparison

| Feature | solar panel lease | solar panel purchase |

|---|---|---|

| Upfront cost | Low or zero upfront | High upfront or financing |

| Ownership | Lessee owns none; system owned by lessor | Buyer owns system |

| Maintenance & repairs | Maintenance often included by lessor | Buyer responsible (within warranty) |

| Tax incentives/credits | Incentives go to lessor or contract terms | Homeowner claims incentives (ITC, state) |

| Long-term cost/value | Higher total payments over term; limited equity | Potentially lower lifetime cost; asset equity |

| Transferability on sale | Lease may transfer with approval | Sale may trigger payoff or ownership transfer |

| Best for | Budget-friendly, flexible timing | Long-term ownership, maximum savings |

Strengths

- Low upfront cost and easier approval for renters

- Predictable monthly payments and maintenance options

- Potentially faster solar deployment with minimal home disruption

- Flexibility to upgrade systems at end of term

Drawbacks

- No ownership or equity in the system

- Higher long-term cost if staying long term

- Transfer complications when selling a home with an active lease

- Possible end-of-term fees or restricted buyout options

Buy for long-term ownership; lease for lower upfront cost and flexibility

Ownership generally yields the best long-term value and equity, especially for stay-at-home homeowners. Leases work well if you need minimal upfront cash and straightforward budgeting, but come with ongoing payments and transfer considerations. Use a side-by-side model to confirm which path aligns with your plans.

Frequently Asked Questions

What is the main difference between a solar panel lease and a purchase?

The main difference is ownership and cash flow. A lease lets you use the system with ongoing payments while ownership remains with the provider, whereas a purchase puts ownership in your hands, with upfront or financed costs. Your choice shapes incentives, maintenance obligations, and long-term value.

Leasing means you pay to use the system; buying means you own it and may gain incentives over time.

Who benefits from the tax credits when leasing?

In most leases, the tax credits go to the system owner or leasing company, not the tenant. Some contracts offer credit transfer options, but terms vary by provider and state. Always verify credit flow before signing.

Usually the owner gets the credits, so ask about transfer options.

Can I switch from a lease to buying later?

Many contracts offer a buyout option or conversion at some point, but terms differ. Consider potential costs, remaining depreciation, and whether the upgrade path aligns with your long-term home plans.

You might be able to switch later, but check the contract for buyout terms.

Is a lease a good option if I plan to sell soon?

If you plan to move within the lease term, evaluate transferability to the new owner, potential penalties, and whether the buyer is comfortable assuming the lease. A lease can complicate resale if transfer options are restrictive.

Leases can complicate selling unless transfer is easy.

What should I look for in a lease contract?

Look for transfer terms, end-of-term options, price escalations, maintenance inclusions, and any penalties for early termination. Also verify performance guarantees and whether the contract ties payments to energy production guarantees.

Check for transfers, costs, and guarantees before signing.

What are common hidden fees in solar leases?

Common fees include early termination charges, transfer fees, escalators, and potential charges for underperformance of the system. Read the entire fee schedule and ask for a breakdown of every line item.

Watch out for extra fees that aren’t obvious at sign-up.

Top Takeaways

- Assess long-term stay in your home before choosing

- Prioritize ownership when you expect rising energy costs

- Check transferability and penalties before signing

- Model total costs, not just monthly payments

- Confirm who gets incentives and how they’re applied