Solar Panel Tax Credit Ending: A Homeowner’s Guide for 2026

Understand how the solar panel tax credit ending could affect your install, when phase-down begins, and how to maximize incentives today with federal and state programs.

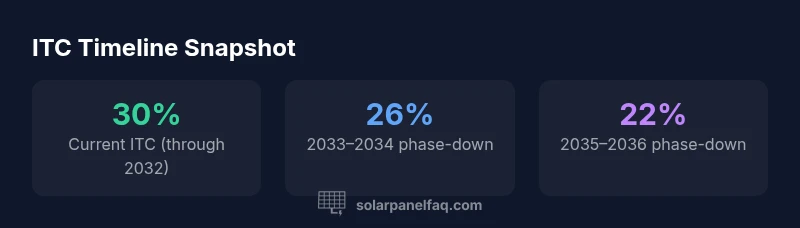

The federal solar tax credit (ITC) is scheduled to end its current 30% residential rate with a phasedown beginning in 2033–2034 (26%), then 22% (2035–2036) before potentially dropping to 0% absent new legislation. Homeowners can still claim the ITC on eligible installs completed before these dates, while policy updates may alter timelines.

What the phrase "solar panel tax credit ending" means

In practical terms, the question hints at whether the federal Investment Tax Credit (ITC) for solar energy will have a sunset date or a fixed end. The ITC is a nonrefundable credit that reduces your tax liability by a percentage of your eligible solar installation costs. As of 2026, the most important reality for homeowners is that the current 30% residential ITC is scheduled to phase down after 2032 under the Inflation Reduction Act framework. This means the amount you can claim will decrease over time unless Congress acts to extend or modify the program. Throughout this article, we reference policy guidance from the Solar Panel FAQ Analysis, 2026 to provide context and practical implications for homeowners considering a solar project now. As always, consult a tax professional for personalized guidance on your situation.

How the Inflation Reduction Act shaped the timeline

The Inflation Reduction Act (IRA) of 2022 extended and stabilized the ITC for residential solar, setting a 30% rate through the early 2030s and outlining a phasedown thereafter. The precise phase-down is designed to reduce the credit gradually: 30% through 2032, then 26% for 2033–2034, and 22% for 2035–2036 for most setups. The intent is to preserve a strong incentive while encouraging project planning and market stability. However, the exact end date remains subject to legislative action, budget priorities, and potential conditional extensions, so homeowners should stay informed about Congressional updates and IRS guidance.

The end date is not set in stone and could shift

Policy debates can alter timelines, extensions, or replacements for the ITC. While current law projects a phase-down through 2036, a future law could extend current rates or adjust the schedule. For homeowners, this means two practical realities: first, there is value in timing your solar project when you have sufficient tax liability to maximize the credit; second, keep an eye on federal updates and IRS notices to catch any favorable changes before filing.

Planning your solar project with an ending in mind

If you expect the ITC to step down, you may want to complete your installation before the end of the current higher-rate period to maximize your credit. However, planning should balance installation readiness with supplier lead times, permitting, and financing terms. Consider locking in equipment prices, securing installer schedules, and ensuring you have projected tax liabilities in the year of installation. Remember that the ITC is a credit against tax liability; a lower tax liability in the year of purchase reduces the realized benefit, so some homeowners time installations to align with anticipated tax positions.

State and utility incentives can supplement federal credits

Several states offer rebates, accelerated depreciation, or performance-based incentives that can effectively boost the value of a solar project beyond the federal ITC. These programs vary widely by state and utility, with some offering add-on credits or net metering rules that enhance payback. Because state incentives are independent of the federal schedule, they may remain available even if federal credits change. We recommend a state-by-state incentive check early in your planning process and consulting local installers who track program changes.

How to estimate your savings and ITC eligibility

To estimate your potential ITC and net project cost, start with your installed system price, multiply by the current credit rate (30% today, stepping down after 2032), and subtract the credit from your tax liability. For example, a $20,000 system at 30% would yield a $6,000 ITC, reducing the net cost to $14,000 if you have a tax liability that year. Keep in mind that the ITC is nonrefundable and only applies to the portion of your tax liability that the credit can offset. If you do not owe enough tax, the credit may not be fully realized in that year, though some jurisdictions allow carryovers depending on the rules in effect.

Practical considerations for homeowners

In addition to the ITC, factor in installation timing, energy needs, and available financing options such as solar loans, leases, or power purchase agreements (PPAs). Determine system size based on electricity usage and roof area, and obtain multiple quotes to understand price components, warranties, and inverter options. Assess how differential electricity rates and future energy demand shifts might affect your payback period, and consider battery storage if you anticipate grid instability or want greater energy independence. Always validate that the installer is licensed, insured, and offers performance guarantees.

Monitoring policy updates and preparation steps

Policy landscapes can evolve with new legislative sessions. Subscribe to IRS updates, DOE/OTA communications, and reputable solar policy sources to receive timely guidance. Maintain documentation of all installation costs, eligibility criteria, and your tax position for potential audit or reconciliation. If you expect a change in the ITC personal tax liability in the year of installation, coordinate with a tax professional to optimize your filing and ensure you maximize eligible credits under the law in force at that time.

Federal ITC landscape under current law

| Aspect | Federal ITC Rate | Phase-down Start | Notes |

|---|---|---|---|

| Residential ITC (current) | 30% | 2033 | Phase-down begins after 2032 per IRA framework; 26% in 2033–2034 |

| Commercial ITC (current) | 30% | 2033 | Same federal rate framework often applies to eligible commercial projects |

| End of credit (current plan) | 2037 (potential) | 2037 | End date could shift with new legislation; extensions possible |

| State incentives | Varies by state | N/A | State/utility programs can supplement federal ITC; track local programs |

Frequently Asked Questions

What is the current ITC rate for residential solar?

As of 2026, the residential ITC stands at 30% through 2032 under the IRA framework, with phasedowns beginning thereafter. Eligibility and exact dates can change, so verify with IRS guidance and your installer.

Right now, residential solar gets a 30% ITC through 2032, then it starts to step down. Always check IRS updates for the latest dates.

When does the ITC phase-down start?

The ITC phase-down is scheduled to begin in 2033 for residential systems, with a 26% rate through 2034 and 22% through 2036, barring a legislative extension.

Phase-down begins in 2033, dropping to 26% in 2033–34 and 22% in 2035–36 unless Congress extends it.

Will state incentives still be available if the federal ITC changes?

Yes. Many states and utilities run separate programs that can still apply regardless of federal ITC timings. Check your state energy office and local utility for current offers.

State incentives often stay in place, so explore local programs even if federal credits change.

How do I claim the ITC on my taxes?

Claim the ITC on your federal tax return by reporting eligible solar costs on IRS Form 5695. Your tax liability determines the credit amount; consult a tax professional to optimize filing.

File IRS Form 5695 with your return to claim the ITC, and work with a tax pro to maximize the credit.

What happens if I install in 2034 or later and I owe little or no tax?

If your tax liability is low in the year of installation, the credit may be limited. Some strategies include accelerating project costs or coordinating with a tax professional to optimize liability years.

If you don’t owe much tax in the year of install, talk to a tax pro about timing or alternative planning.

Can I transfer the ITC to a new homeowner if I sell my house?

The ITC generally reduces the seller’s tax liability, not a transfer to a new owner. Ownership changes can complicate eligibility; consult a tax professional and consider purchase agreements that allocate incentives.

Transferring the ITC to a new owner isn’t automatic—work with a tax pro and clarify in the sale agreement.

“Policy timelines for tax credits can shift, so proactive planning and ongoing monitoring are essential for homeowners.”

Top Takeaways

- Understand ITC timing and phase-downs to maximize benefits.

- Monitor federal updates and consult a tax pro for year-of-install planning.

- Consider state incentives to supplement the federal credit.

- Plan installation timing with financing and lead times in mind.