Who Is Solar Panel Funding? A Homeowner's Guide to Financing

Explore who funds solar panel installations—from lenders to government programs. Learn loans, leases, PPAs, and incentives, and how funding choices impact cost and payback for homeowners.

Who is solar panel funding? The capital for solar installations comes from a mix of lenders, installers, government programs, and energy providers. Typical options include cash purchases, solar loans, leases, PPAs, and incentives. Understanding who funds solar helps homeowners compare ownership models, upfront costs, and long-term savings, enabling a more informed decision about solar investment.

What is solar panel funding and who is funding it?

In plain terms, solar panel funding refers to who provides the capital to purchase and install solar panels. The pool includes traditional lenders such as banks and credit unions, specialized solar finance companies, and energy providers that offer financing as part of a broader energy service. Public programs and government incentives also contribute, either directly or indirectly, by reducing net costs or offering rebates. Solar installers may participate in financing arrangements to help customers move from consideration to installation. For homeowners, understanding who is funding solar helps you compare ownership models (own vs. lease/PPAs), evaluate upfront costs, and project long-term savings with greater confidence. According to Solar Panel FAQ, the funding ecosystem is increasingly a mix of consumer credit, manufacturer partnerships, and policy-driven incentives, which collectively shape the affordability and accessibility of solar.

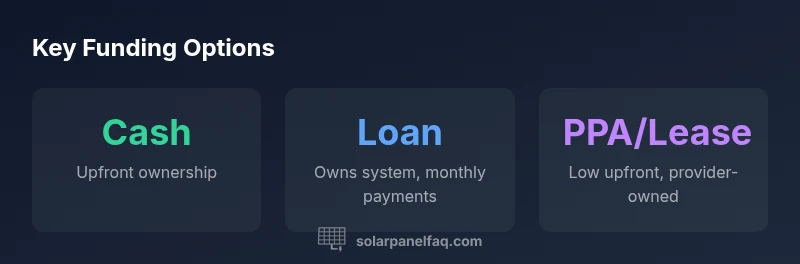

Common funding pathways include cash purchases, unsecured or secured solar loans, solar leases, and Power Purchase Agreements (PPAs). Each path has distinct implications for ownership, maintenance responsibility, tax incentives, and monthly payments. Cash purchases maximize long-term savings and allow immediate ownership, but require a larger upfront investment. Loans spread the cost over time, allowing ownership with predictable monthly payments. Leases and PPAs reduce or eliminate upfront costs but transfer ownership or long-term energy rights to a provider, while incentives, credits, and rebates can dramatically alter the economics of any option. Homeowners should model multiple scenarios using their current electricity rates, expected future rates, and available incentives to determine the most cost-effective approach.

Financing options for homeowners

There is no one-size-fits-all solution for financing solar; the best choice depends on your goals, credit profile, and property. Here, we break down the most common options and how they affect ownership and cost over time:

- Cash purchase: pays for the system upfront, maximizing lifetime savings and ownership. Requires substantial initial capital but yields the highest net value when incentives are included.

- Solar loan: funds the system and repays over 5–20 years with interest. Ownership remains with the homeowner, and you can still claim incentives and enjoy energy savings from day one.

- Solar lease: the system is owned by a third party. You pay a fixed monthly lease payment, often without maintenance duties, but long-term energy ownership sits with the lessor.

- Power Purchase Agreement (PPA): you buy electricity instead of the system itself. Payments are typically based on a per-kWh price and may include maintenance; ownership remains with the provider.

- Hybrid approaches: some homeowners combine a smaller down payment with a loan, or opt for a PPA with performance-based incentives.

When evaluating these options, consider total cost of ownership, maintenance responsibilities, contract length, escalation clauses, and who is eligible for tax credits or rebates. The goal is to align financing with your energy goals, risk tolerance, and expected home improvements. Solar Panel FAQ’s data shows that many homeowners choose a mix of options to balance upfront affordability with long-term benefits, especially where incentives are strongest.

Government incentives and utility programs

Public programs and utility-based incentives play a pivotal role in solar funding. Federal tax credits, state rebates, and local incentives can dramatically lower the net cost of solar, sometimes reducing upfront expenditure by a substantial margin. Net metering policies and export credit schemes affect the value of generated electricity, potentially improving payback periods. In addition, some regions offer grants, low-interest loans, or performance-based incentives tied to system performance, installation date, or local solar adoption goals. To maximize value, homeowners should verify current incentives in their jurisdiction, understand application timelines, and recognize that programs can change with policy updates. Solar Panel FAQ emphasizes consulting a trusted advisor to map available incentives to your financing plan and to avoid missing opportunities caused by policy misalignment.

Cost considerations and payback: estimating value

A clear understanding of cost and payback is essential for credible solar budgeting. The upfront cost is only part of the story; incentives, maintenance, and energy price trends drive the true economics. A typical homeowner should model:

- Upfront costs after incentives (if any)

- Annual energy savings based on local sun exposure and household usage

- Annual increases in electricity rates and any rate caps in your region

- System degradation over time and potential maintenance costs

- Financing costs (interest, fees) if not purchasing with cash

Shipping, installation complexities, roof condition, and permitting fees can add to the total. By running multiple scenarios—cash, loan, lease, and PPA—you can compare the real payback period and total lifetime cost. The Solar Panel FAQ analysis suggests payback periods generally improve with higher sunshine, larger system size, and stronger incentives.

How to choose the right funding path for your home

Choosing the best funding path starts with a clear assessment of your goals and constraints. Use this practical checklist to decide:

- Ownership preference: Do you want maximum long-term savings and asset ownership, or lower monthly payments with limited maintenance responsibilities?

- Cash flow: Can you comfortably cover a down payment or potential loan payments without compromising other priorities?

- Incentives: Are you located in a region with strong incentives that favor ownership or certain financing structures?

- Home characteristics: Roof orientation, shading, and existing attic space affect system size and cost, influencing financing choices.

- Risk tolerance: Are you comfortable with loan interest rate fluctuations or contract terms that bind you for 15–25 years?

Create a side-by-side comparison in a simple table or spreadsheet, covering upfront costs, monthly payments, maintenance responsibilities, contract length, and net present value. Solar Panel FAQ’s framework recommends measuring Total Cost of Ownership (TCO) rather than just the upfront price to capture the full value of your decision.

Practical steps to compare offers and avoid pitfalls

To compare offers effectively and avoid common pitfalls, follow this practical workflow:

- Gather multiple quotes from reputable installers and lenders. 2) Verify all incentives and assess how they affect each financing option. 3) Read every contract term—length, escalators, maintenance obligations, and transferability. 4) Use a standardized calculator to estimate payback under each option. 5) Check for hidden fees, prepayment penalties, or service limitations. 6) Confirm roof condition and permitting costs, which can alter the economics. 7) Request references or reviews on the installer’s service quality and warranty terms. 8) Consider a post-installation performance check to validate projected energy production. Solar Panel FAQ notes that transparent, apples-to-apples comparisons help homeowners avoid surprises later in the contract.

The future of solar funding: trends to watch

Funding for solar continues to evolve as technology improves and policy landscapes shift. Expect increasing use of flexible financing products designed to lower entry barriers for homeowners, such as blended loans, energy-as-a-service models, and performance-based incentives. As solar becomes a standard home upgrade, demand for simple, clear, and transparent financing terms will grow, prompting lenders and installers to offer bundled solutions that combine design, permitting, installation, and ongoing maintenance. Regulators may also simplify eligibility criteria for incentives, making it easier for homeowners to participate. Solar Panel FAQ predicts a continued push toward consumer-friendly funding options that balance affordability with long-term energy resilience.

Overview of common solar funding options

| Funding Option | Typical Terms | Who Qualifies | Best For |

|---|---|---|---|

| Cash purchase | Upfront payment; maximum savings | Any homeowner with capital | Maximize lifetime savings and ownership |

| Solar loan | 5-20 year terms; interest varies | Credit applicants | Owns system with manageable payments |

| Lease | Fixed monthly payments; maintenance often included | Property owners or leasing entities | Low upfront cost, minimal maintenance |

| PPA | Pay per kWh; contract length 15-25 years | Homeowners seeking predictable energy costs | No ownership, predictable bills |

Frequently Asked Questions

What is solar panel funding?

Solar panel funding refers to the different ways homeowners pay for solar installations, including cash, loans, leases, PPAs, and incentives. Each option has implications for ownership, maintenance, and payback.

Solar panel funding means choosing how you pay for the system and who owns it.

Who typically funds solar panels?

Funding comes from lenders, solar installers, manufacturers’ financing programs, and government incentives. Utilities may also offer programs that reduce net costs.

Lenders, installers, and government programs typically fund solar installations.

What is PACE financing and who can use it?

PACE financing is repaid via property taxes and is available in many regions for homeowners and some commercial properties, depending on local programs and eligibility.

PACE lets you pay over time through your property taxes.

Do incentives affect funding choices?

Yes. Incentives can significantly lower effective costs, shorten payback, and improve the overall return on investment for any funding path.

Incentives make solar more affordable and can shorten payback.

Can renters access solar funding?

Renters typically cannot own the system; leases and PPAs are common options that let a third party install and maintain a system while the renter benefits from cheaper electricity.

Renters usually use leases or PPAs to access solar benefits.

What should I look for in a financing contract?

Look for contract length, transferability, escalation, maintenance responsibilities, and clearly defined incentives or rebates.

Check the fine print: length, costs, and who handles maintenance.

“Financing a home solar system is as much about long-term value as it is about upfront cost. A rigorous comparison of ownership, maintenance, and incentives leads to the most cost-effective choice.”

Top Takeaways

- Start with your goals: ownership vs. predictable payments.

- Model multiple funding paths to see true payback.

- Incentives dramatically alter economics; verify eligibility.

- Compare apples-to-apples with standardized cost analyses.

- Review contract terms for ownership transfer and maintenance responsibilities.